404: Adoption Not Found

The CLARITY Act's Section 404 addressed the wrong stablecoin problem.

The Yield Fight Misses the Point

On May 14, the Senate Banking Committee advanced the CLARITY Act, a major step toward a U.S. market structure framework for digital assets. But one of the most important fights was Section 404: the compromise over stablecoin yield.

Stablecoins are digital dollars backed by reserves, often Treasury bills and other safe assets. Those reserves earn interest. The political fight was simple: can holders profit from that revenue?

Banks argued that yield-bearing stablecoins would look like deposits without bank regulation. Crypto companies argued that consumers should not lose access to rewards simply because banks want to protect their deposit base.

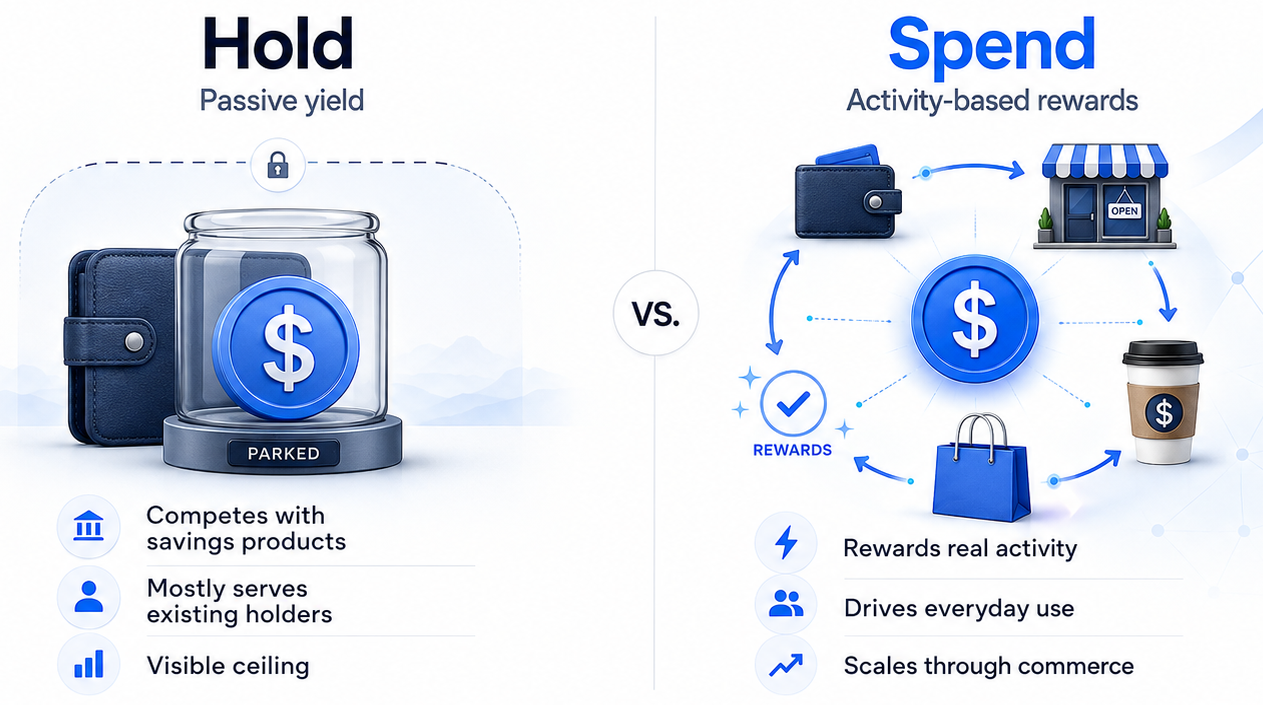

The compromise, brokered by Senators Thom Tillis and Angela Alsobrooks, draws a line between passive yield and activity-based rewards. Platforms would be restricted from paying interest-like returns on idle stablecoin balances. Rewards tied to actual usage, including purchases, referrals, merchant rebates, loyalty programs, and promotional campaigns, remain permitted.

That distinction is not yet final. But if it survives markup, the adoption path it implies is clear. Stablecoin rewards need to be tied to activity: a purchase, a referral, a merchant rebate, a loyalty campaign, or another measurable use.

That is not a constraint on adoption. It is the adoption map. Stablecoins will not become mainstream because people are paid to hold them. They will become mainstream when people have useful reasons to use them.

Issuer-Funded vs Merchant-Funded Incentives

The question now is not whether rewards survive. It is who should fund them, and what behavior they should create.

Stablecoin issuers already have a powerful business model: issue digital dollars, hold reserves, and earn income on those reserves. Tether reported more than $10 billion in 2025 profit. Circle reported $2.7 billion in 2025 revenue. The strategic question is whether issuers should spend that income subsidizing user adoption, or preserve it and let merchants fund the rewards that create actual commerce activity.

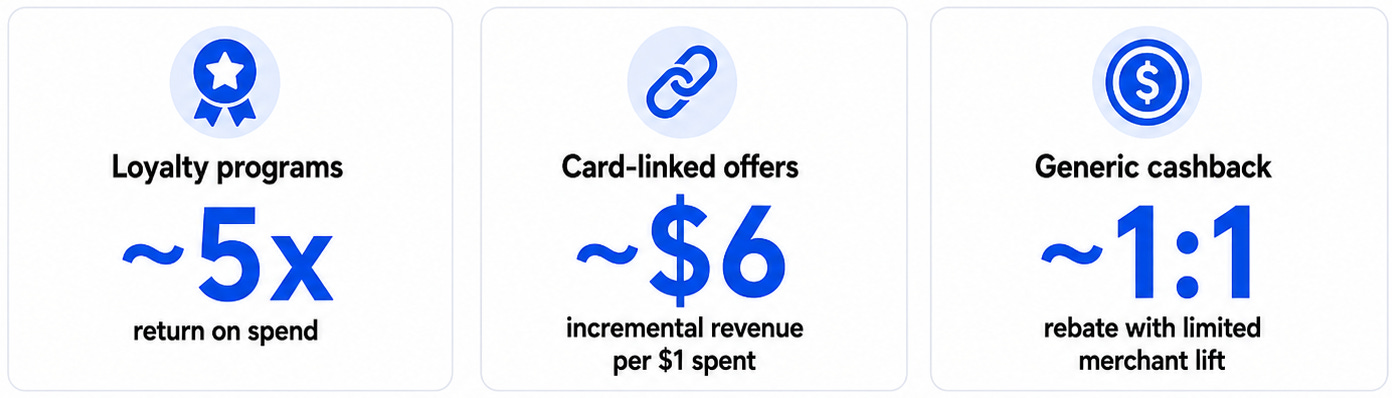

The obvious move looks like issuer-funded cashback. The UX is simple. Fintech has already proven the playbook. But issuer-funded cashback is a pure subsidy: it generates transactions without generating signal. One dollar of cost produces one dollar of activity with no information about whether the customer would have transacted anyway. And as more issuers enter the market, cashback rates converge and margins compress. The subsidy becomes table stakes rather than a growth engine.

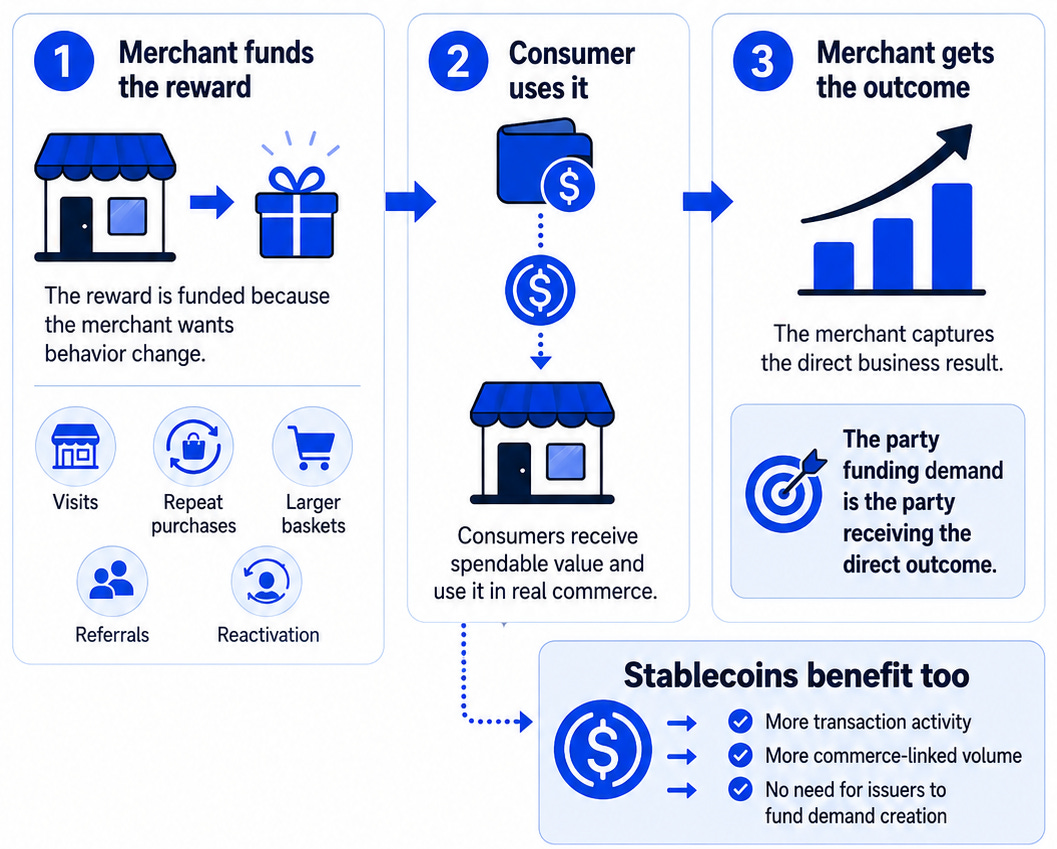

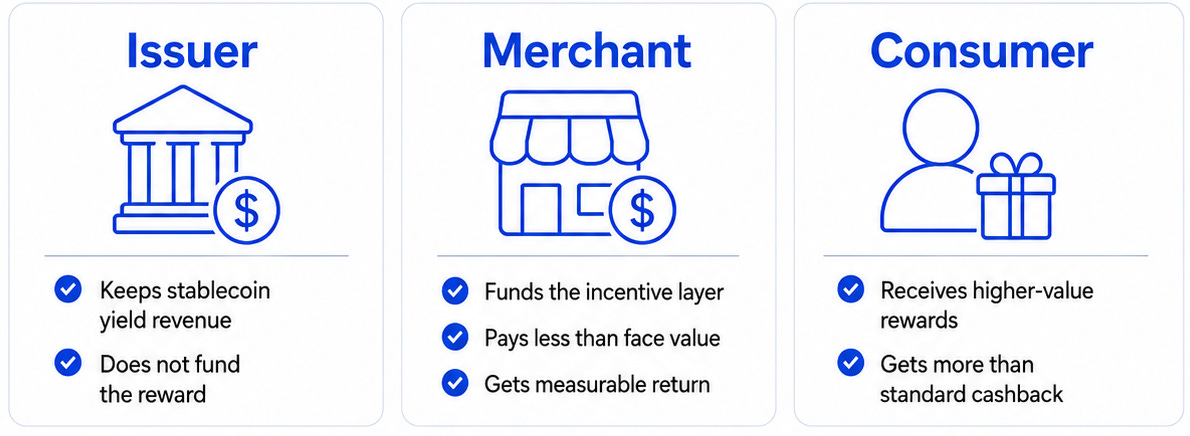

The better path is merchant-funded rewards, because merchants already have a business reason to pay for visits, repeat purchases, referrals, larger baskets, and customer reactivation. Merchants are not funding rewards to promote stablecoins. They are funding rewards to drive revenue. Stablecoins benefit because the activity is real, funded by the party with a direct business outcome, not subsidized by the issuer.

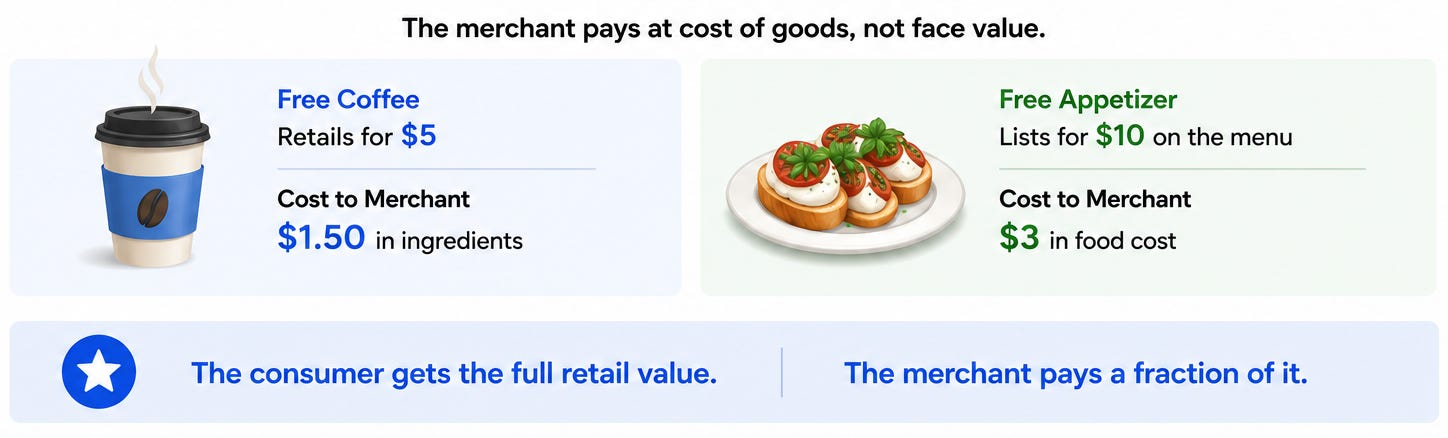

It is also more efficient than generic cashback. Cashback is simple, but it has limited economic leverage: one dollar of issuer cost usually becomes one dollar of consumer value. Merchant-funded rewards work differently because the merchant’s cost is often below the reward’s retail value.

A $5 coffee may cost the merchant $1.50. A $10 appetizer may cost $3. The consumer feels the full retail value, while the merchant pays closer to cost. That is why merchant-funded rewards can feel more valuable than cashback without requiring the issuer to fund the entire incentive.

That changes the economics. Consumers get rewards worth using. Merchants get measurable sales impact. Issuers can use the system to motivate both sides to adopt their stablecoin and, importantly, preserve the yield.

Driving Real Stablecoin Adoption

The stablecoin industry has spent years building rails: issuance, custody, wallets, compliance, liquidity, acceptance, and settlement.

Those rails are necessary but not sufficient. They do not create demand.

They cannot, by themselves, make a customer choose one merchant over another, make a small business fund an offer, or prove which reward changed behavior.

Issuers, wallets, exchanges, and payment companies need everyday usage beyond trading, treasury, and crypto-native flows. Many already have reach. The missing piece is activation. Turning distribution into adoption requires a commerce incentive layer.

Traditional loyalty has not solved this either. Most programs live inside one merchant at a time. Value gets trapped, engagement fades, and merchants have no way to measure whether the incentive actually changed behavior.

Tens of billions of dollars have flowed into 600+ stablecoin and stablecoin-adjacent companies over the past few years. Their survival now depends on accessing the incentive layer.

How Issuers Can Leverage Twism

A stablecoin issuer looking at this today needs three things it does not have internally: a live merchant network funding real offers, a consumer base redeeming them, and a measurement layer proving which incentive changed behavior.

Twism already has all three. More than 5,000 onboarded merchants, more than 156,000 consumers, and millions of transaction records, giving stablecoin issuers and payment partners a live commerce network to build on. Its distribution partnership with North will soon expand that reach to more than one million merchant locations.

Merchants use Twism to fund rewards tied to specific outcomes: visits, repeat purchases, larger baskets, referrals, and reactivation. Consumers receive spendable value. Twism measures whether the incentive worked.

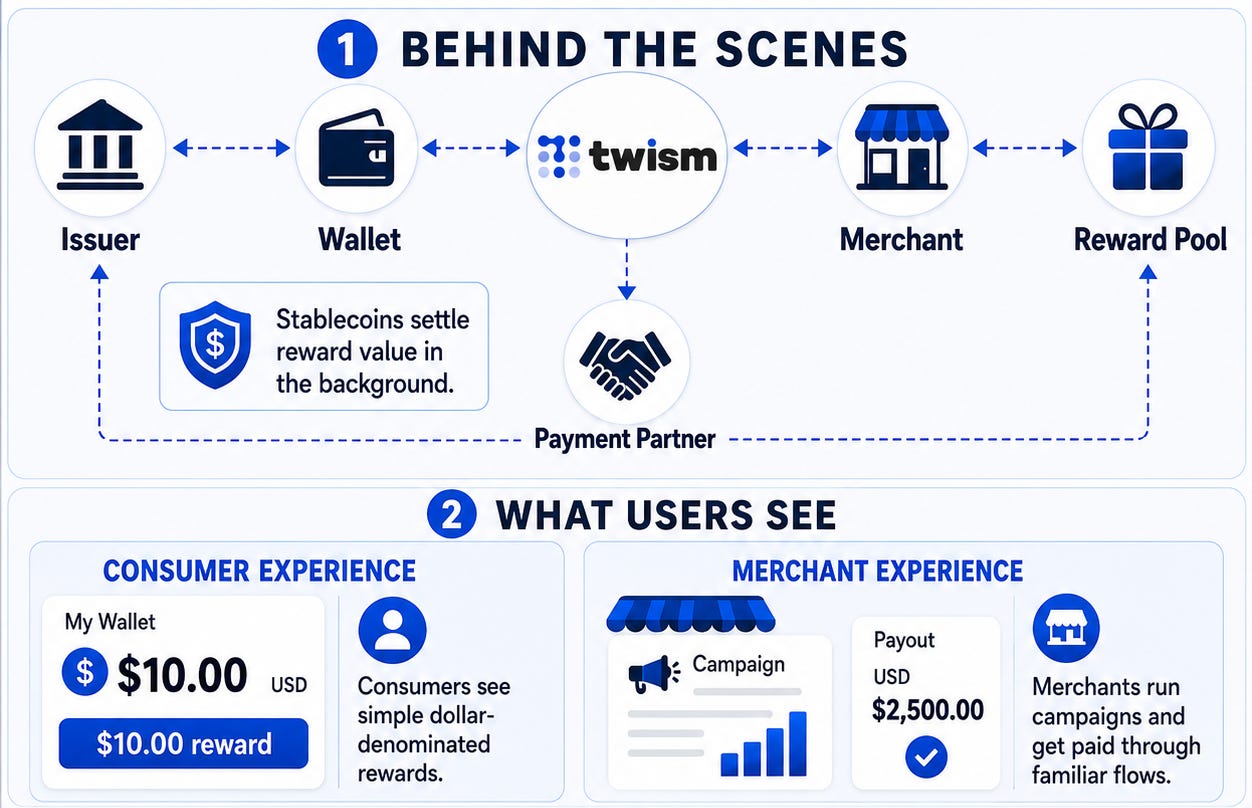

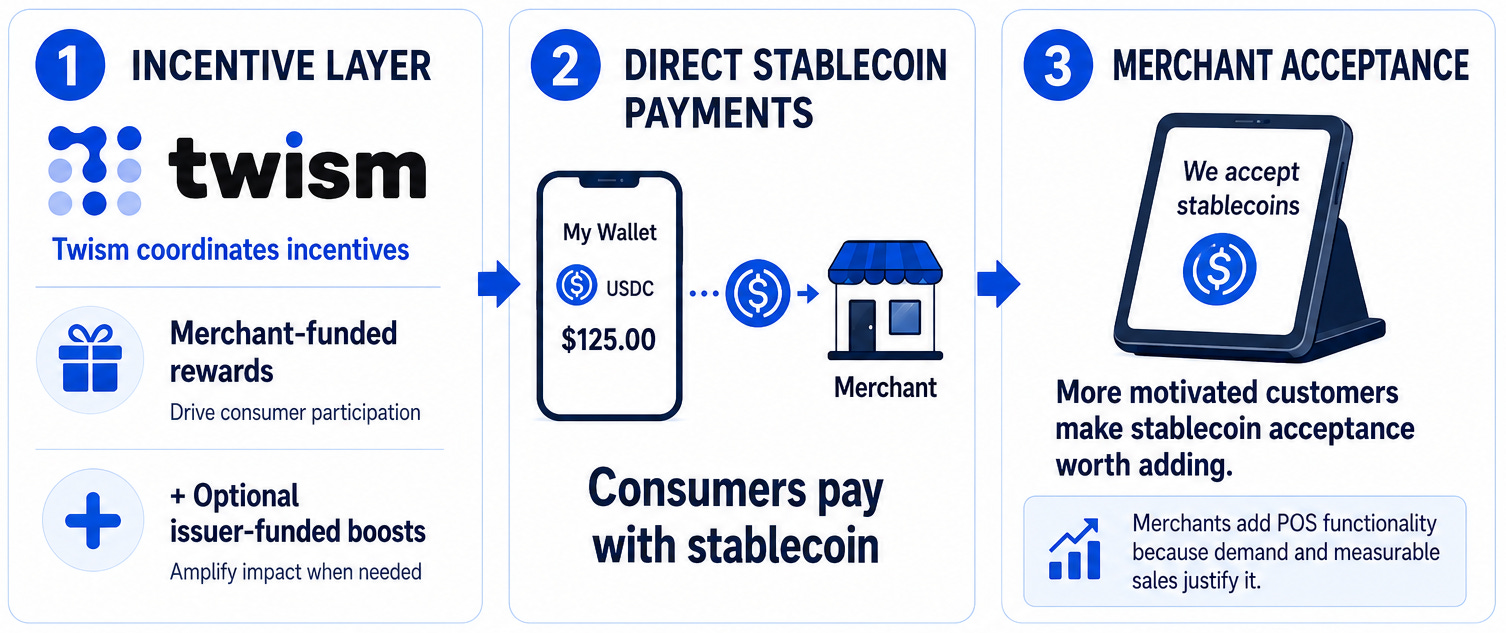

While Twism is payment rail-agnostic, it creates the ideal incentive layer for stablecoin issuers to reward consumers for paying with their specific stablecoin and merchants for accepting it.

And although most merchant front ends are not yet ready to accept stablecoin payments, there is a practical near-term application in the backend.

For example, an issuer could partner with Twism to settle reward redemptions using its stablecoin. Consumers would still see simple dollar-denominated rewards. Merchants would still run familiar campaigns. The stablecoin improves the plumbing without becoming the headline.

Over time, as wallets, POS systems, compliance, and merchant readiness improve, backend settlement can expand into direct stablecoin payments. Twism gives issuers a practical path to that transition: merchant-funded rewards give consumers a reason to pay with stablecoins, while issuer-funded boosts can increase the incentive where needed.

For merchants, stablecoin acceptance stops being a technical upgrade and becomes a growth channel: a way to attract motivated customers and drive measurable sales.

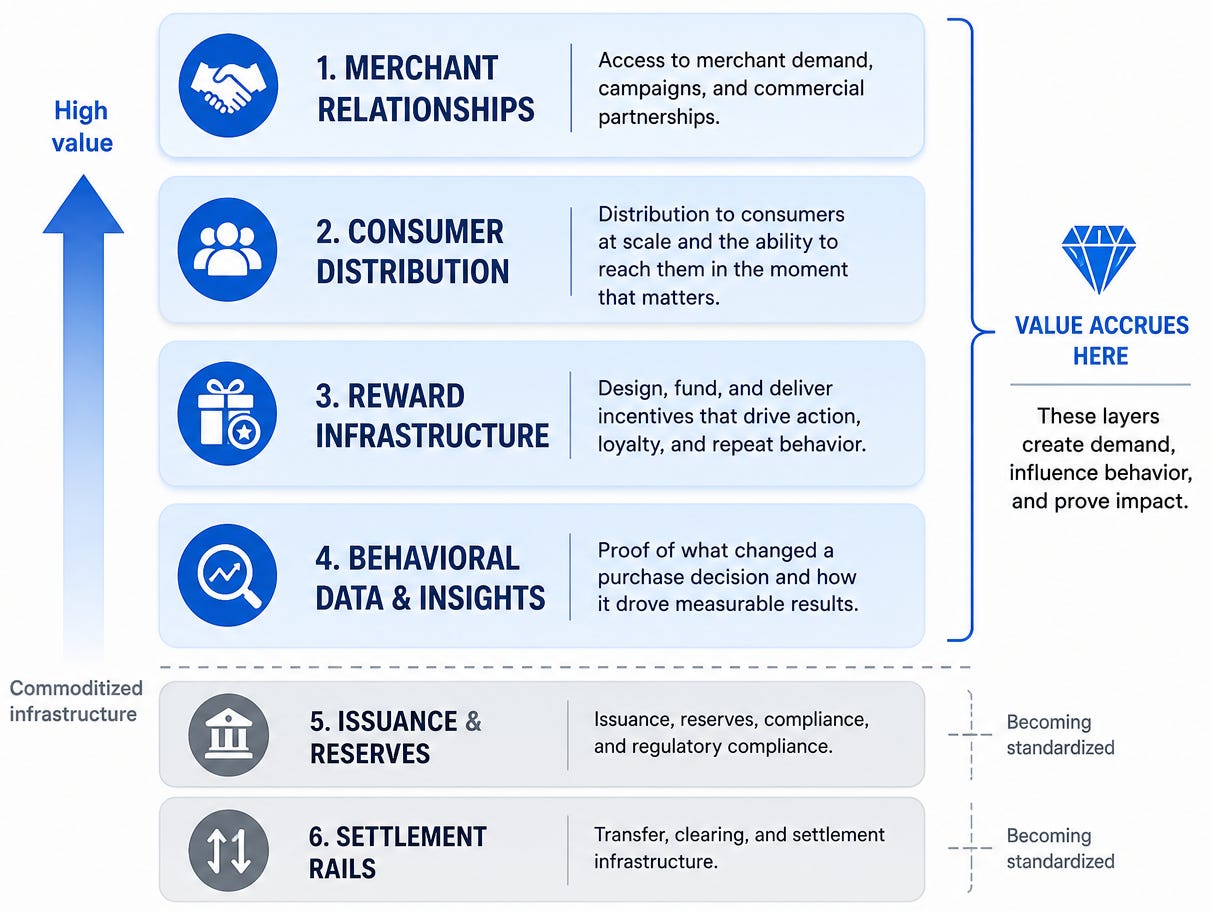

Value Capture in the Stablecoin Stack

The stablecoin market is separating into two layers: issuance, meaning who creates the digital dollar, holds the reserves, satisfies regulators, and earns the spread, and usage, meaning who turns those dollars into everyday transactions.

Section 404 points the market toward the second layer. If rewards are tied to activity, the market will need systems that create and measure that activity.

That changes where value accrues.

As issuance and settlement become standardized, value increasingly depends on what happens above the rails: merchant relationships, consumer distribution, reward infrastructure, and the data showing what changed a purchase decision. Issuers who attach to an incentive layer gain a structural advantage over those competing on spread alone.

The winner will not be the company that pays people the most to hold digital dollars. It will be the company that gives people the best reason to spend them.

Disclosure: I’m the Chief Strategy Officer at Twism. This piece reflects my personal view. Legislative references are based on the Senate Banking Committee substitute released May 12, 2026, and may change as the bill advances.